|

22.01.2020 14:35:17

|

Janus Henderson Investors: Early 2020 money data key for global outlook

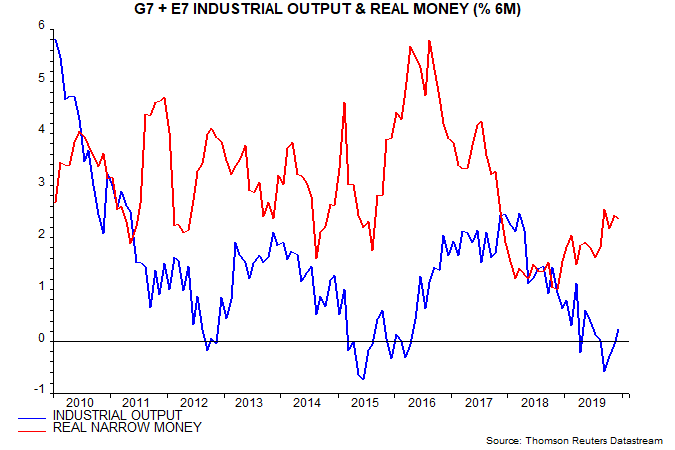

Based on monetary data covering 70% of the aggregate and near-complete CPI inflation data – see first chart.

Real money growth remains well below a post-GFC average of 3.2%, suggesting that six-month industrial output momentum will show limited recovery through Q3 2020, allowing for an average nine-month lead.

Real money growth bottomed at 1.0% in November 2018 while industrial output momentum appears to have reached a low 10 months later in September 2019.

The recent high for real money growth was 2.6% in September 2019. A rise through this level, ideally to 3-4%, in early 2020 would signal economic acceleration during H2 and into 2021. This is the scenario suggested by cycle analysis – the stockbuilding and business investment cycles are expected to have entered recovery phases by H2.

A relapse in real money growth without a prior breach of the September high, however, would signal a “double dip” starting around mid-2020.

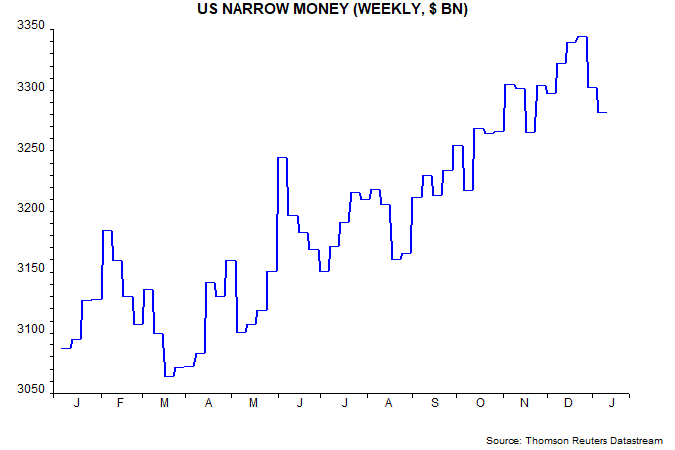

US trends could drive a relapse. Six-month narrow money growth surged higher in September as the Fed cut rates for the second time in two months and restarted balance sheet expansion – second chart. Rates have been stable since end-October and the balance sheet boost could be ending. Narrow money contracted in the first two weeks of January – third chart.

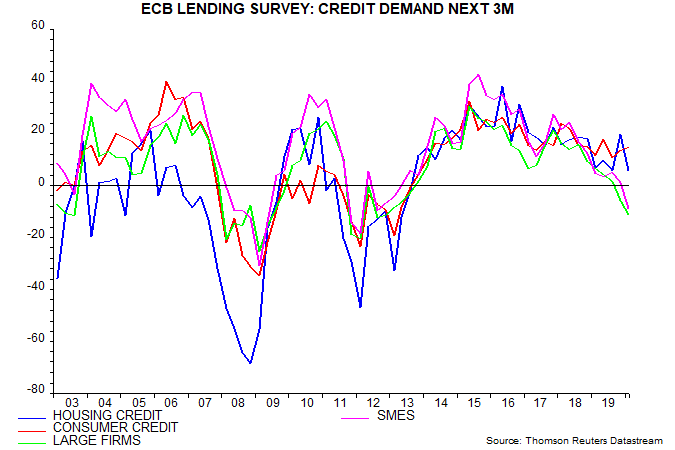

A fading impact of the ECB’s September policy easing could similarly result in a moderation of Euroland money growth. The Q4 bank lending survey released today signalled a further weakening of business credit demand – fourth chart. (December money numbers will be released on 29 January.)

An alternative positive scenario is that US / Euroland money trends remain solid while a reversal of recent Chinese real money contraction pushes the global six-month growth measure through 3%. A sharp fall in CPI inflation as pork prices normalise will give a significant boost to Chinese real money but the timing is uncertain, while – as previously discussed – a recovery in nominal money growth probably depends on an unwind of bank credit tightening during 2019, of which there is little sign yet.

powered by

Der finanzen.at Ratgeber für Fonds!

Der finanzen.at Ratgeber für Fonds!

Wenn Sie mehr über das Thema Fonds erfahren wollen, finden Sie in unserem Ratgeber viele interessante Artikel dazu!

Jetzt informieren!

Fondsfinder

Letzte Top-Ranking Nachrichten

Oskar ist der einfache und intelligente ETF-Sparplan. Er übernimmt die ETF-Auswahl, ist steuersmart, transparent und kostengünstig.